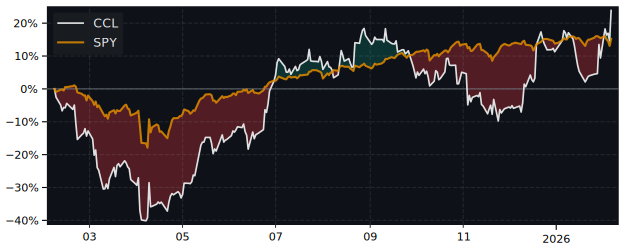

CCL Performance: 58.8% Return (12 Months)

CCL returned 58.8% over 12 months, outperforming the S&P 500 (32.1%). Volatility: 53.2%.

| P/E Trailing | 11.3 |

| P/E Forward | 11.4 |

| 52 Week High | 33.83 USD |

| 52 Week Low | 16.35 USD |

| VRO Trend Strength ±100 | 36.89 |

| Buy Signal ±3 | 0.27 |

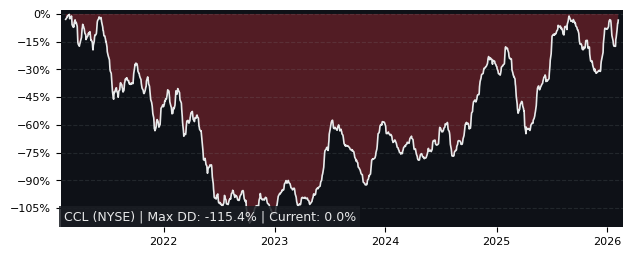

| Max Drawdown | 42.85% |

| Mean Drawdown | 13.50% |

Top Performer in Hotels, Resorts & Cruise Lines (5/29)

| SYMBOL | 1W | 1M | 3M |

|---|---|---|---|

| TH | 47.24% | 73.95% | 69.40% |

| MEL | 5.40% | 24.19% | 23.11% |

| LIND | 5.24% | -2.02% | 20.89% |

| PRSU | 9.01% | 4.80% | 13.60% |

| WH | 3.96% | 9.13% | 4.85% |

| CCL | 8.39% | 0.70% | -19.23% |

| SYMBOL | 6M | 12M | 5Y |

|---|---|---|---|

| LIND | 40.18% | 117.68% | -3.80% |

| VIK | 23.02% | 115.11% | 181.38% |

| TH | 73.95% | 112.81% | 305.36% |

| MEL | 30.54% | 69.67% | 56.03% |

| HTHT | 35.37% | 69.05% | 1.00% |

| CCL | -10.31% | 58.80% | -8.65% |

| SYMBOL | MCAP | 1M | 12M | 5Y | P/E | P/E fwd | PEG | EPS stab | EPS cagr |

|---|---|---|---|---|---|---|---|---|---|

| IHG NYSE InterContinental Hotels |

20.0B | 1.69% | 39.3% | 107% | 27.6 | 22.2 | 1.25 | -37.3% | -53.3% |

| EXPE NASDAQ Expedia |

27.6B | -8.24% | 65.1% | 32.6% | 23.0 | 11.8 | 0.80 | 7.10% | -35.7% |

Performance: CCL vs S&P 500

| PERIOD | CCL | S&P 500 | DIFFERENCE |

|---|---|---|---|

| 1 Month | 0.70% | -1.73% | 2.47% |

| 3 Months | -19.23% | -4.49% | -15.43% |

| 6 Months | -10.31% | -1.33% | -9.10% |

| 12 Months | 58.80% | 32.14% | 20.17% |

| 5 Years | -8.65% | 72.70% | -47.10% |

CCL Performance FAQ

Does CCL outperform the market?

Yes, CCL significantly outperforms the market. Over the past 12 months, CCL returned 58.80% compared to 32.14% for the S&P 500.

What is the CCL return over the last 12 months?

CCL has returned 58.80% over the past 12 months, including dividends. Over 3 months the return was -19.23%, and over 5 years -8.65%.

How risky is CCL?

CCL has relatively low risk with a maximum drawdown of 42.85% over the past 3 years. The average drawdown is 13.50%.

CCL vs Sectors (12m)

Sorted by outperformance. Positive = CCL beats sector.

| SECTOR | ETF | DIFFERENCE 12M |

|---|---|---|

| Consumer Staples | XLP | 49.3% |

| Health Care | XLV | 48.1% |

| Real Estate | XLRE | 45.1% |

| Financials | XLF | 43.9% |

| Consumer Discretionary | XLY | 37.1% |

| Consumer Discretionary | XLY | 37.1% |

| Communication Services | XLC | 29.3% |

| Materials | XLB | 25.2% |

| Industrials | XLI | 16.7% |

| Technology | XLK | 8.8% |

| Energy | XLE | 1.4% |

CCL vs Asset Classes (12m)

| ASSET CLASS | ETF | DIFFERENCE 12M |

|---|---|---|

| S&P 500 | SPY | 20.17% |

| Gold | GLD | 2.6% |

| Long-Term Bonds | TLT | 58.2% |